TWO SIDES OF THE SAME COIN.

Two recent hot topics for buy and sellside firms have been monitoring Execution Quality (TCA) and Market Abuse (MAD). Darren Toulson, head of research at Liquidmetrix explains how they are inextricably linked.

TCA and MAD are usually seen as distinct activities, often implemented in different ways using different systems and procedures. But in essence, the consequence of successful market abuse by one participant will often manifest as poor execution performance for their victims. The patterns of behaviour we’re looking for in TCA and MAD are often the same with the TCA ‘victim’ being one side of the trade and the MAD ‘perpetrator’ being the other side. Let us illustrate with an example.

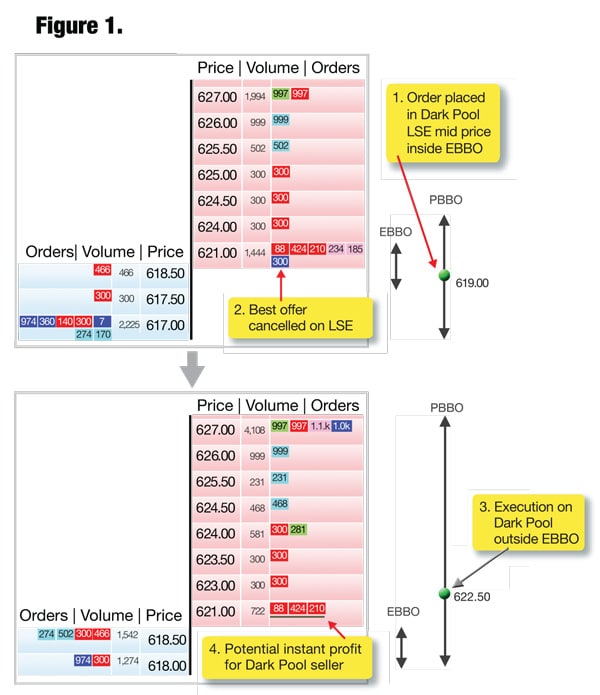

Market manipulation of a reference price to create an instant trading profit?

The diagram shows a pattern of trading activity that, depending on the participants involved, might illustrate market abuse as well as poor execution quality. The example is real and detected in early 2014 using purely public market data – we don’t know who the participants involved are.

To explain what happens (see Fig 1):

- At some time before 10:47:15.643 a buy order for a UK stock is placed on a primary mid-point matching Dark Pool.

- At 10:47:15.643 the lit order books for this stock are shown. The primary market (LSE) best bid and offer price is 617.0/621.0p (blue squares) and the market wide EBBO is similar at 618.5/621.0p.

- At that instant, a liquidity provider with 300 shares resting on LSE at a price of 621.0 cancels their order, causing the LSE bid/offer price to move to a ‘lopsided’ bid offer. The LSE mid-price at this instant lies outside of EBBO so is not really a ‘fair’ market price.

- 19 ms after the LSE order is cancelled, a trade occurs on the Dark Pool for 300 shares at a lopsided LSE mid price (the order book state is shown in the bottom chart).

- Immediately after the Dark Pool trade it’s possible for the seller in the Dark Pool to make an instant profit by buying back immediately on an MTF.

What does this mean from a TCA/MAD perspective?

The buyer with a resting order on the dark pool obtained very poor performance. The intention of using a dark pool is to receive a fair mid-price match with a counterparty; instead the execution occurred at an instant when the LSE mid-price has been distorted by a single market event. No matter what the identities/intentions of the other participants, this trade is problematic for the dark pool buyer from a TCA point of view.

From a MAD point of view, if the trader who cancelled the buy order on the LSE is the same participant who then sent a sell order to the dark pool to trade at the inflated price, then this could be seen as an attempt to profit by causing a reference price to alter. Alternatively, if this was not the intention, or indeed if the participant cancelling the order and the participant selling to the dark pool are different, then this may simply be a ‘fortunate accident’ from the point of view of the dark pool seller. However, the timing of the events and the fact that the same volume cancelled on LSE was then immediately traded at a better price (for the seller) in the dark suggests further investigation may be warranted.

Summary

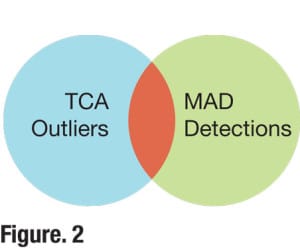

TCA and MAD really are two sides of the same coin: for any abuse to be successful, someone should have poor execution and someone else should make a profit. To illustrate this, figure 2 shows detectable poor TCA performance as one circle and all cases of suspected market abuse as another circle.

- Most poor TCA performance probably has nothing to do with market abuse and is simply down to bad execution strategies.

- Likewise, many potential market abuse patterns lead to no obvious systematic trading loss to other participants. In this case, they are more likely to be artefacts of valid trading styles rather than intentional abuse.

- There is an overlap (red) where a pattern of potentially abusive behaviour by a participant leads directly to poor trading performance for their counterparty victims.

To reduce false alarms, MAD systems can use TCA style analysis to help concentrate on the relatively small intersection of potentially abusive behaviours that lead to actual trading losses for other participants. TCA systems likewise should try to determine if root causes of poor performances correspond with potentially abusive trading activity by other participants so action might be taken to avoid such scenarios.

© Best Execution 2014