ADOPTION OF CRYPTO ASSETS INTO THE INSTITUTIONAL MAINSTREAM.

By Sean K. Ristau, Co-Chair Digital Currency/Blockchain Working Group, FIX Trading Community and Director of Exchange Integration and Education, Bcause LLC & Jim Northey, Co-Chair Global Technical Committee and Co-Chair High Performance Working Group, FIX Trading Community.

Revenue generated from crypto exchanges could more than double to $4bn this year, according to a recent Sanford C. Bernstein & Co report. The analysts believe there are a plethora of opportunities for traditional firms, especially seeing as the buying and selling of digital currencies generated $1.8bn of fees at the largest crypto exchanges last year, or about 8 percent of the revenue seen on traditional exchanges.

The FIX Trading Community Digital Currency Working Group was set up to review both the potential opportunities and impediments facing institutional investors’ involvement in crypto assets. Indeed at a recent FIX Trading Community event held in Chicago, candid discussions were had about why there aren’t more banks, hedge funds, proprietary trading firms and large institutional players in the space today.

State of play

The take-up of crypto assets has been varied, with institutional investors and banks at a current disadvantage because of custody issues, challenges regarding technical infrastructure, and unclear regulatory guidance.

One of the challenges for the institutional investor is the different set of custody requirements that need to be considered when dealing with institutional money rather than retail flow. Due diligence needs to be completed, yet given the sheer number of crypto assets being released it is extremely hard to decipher legitimate offerings.

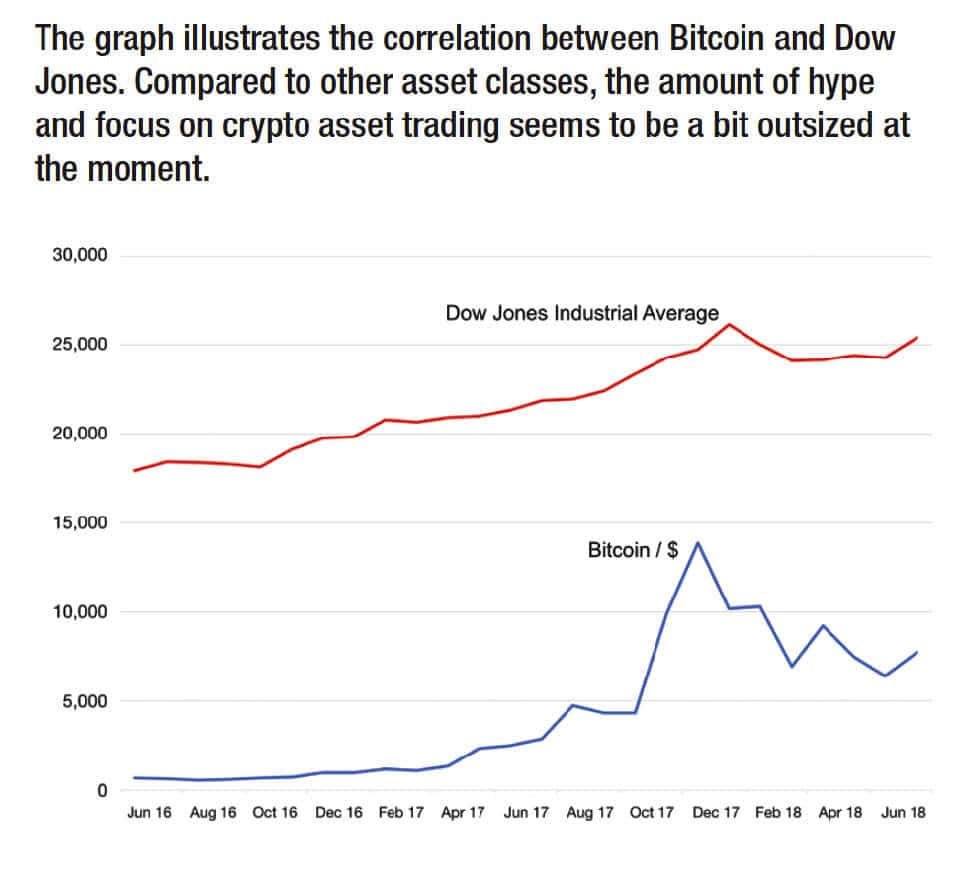

In the meantime, while High Frequency Trading (HFT) firms have adopted and added strategies for crypto, they are still approaching the asset class with caution. HFT firms require an infrastructure not traditionally found in retail exchange setups, therefore they have had to scale back and work with what the exchanges can currently meet until the market matures.

Adoption by proprietary trading firms has been enthusiastic, especially in financial centres such as Chicago and in the Asia Pacific region. Most prop firms we have spoken to are either already trading in crypto, or working on a solution to enter the market. Because of their role as market makers with readily available liquidity, many of the traditional prop firms have entered into the space in both an OTC and market making capacity, providing a great source for liquidity.

Banks and larger institutions such as exchanges and clearing houses, on the other hand, are tending to focus on what blockchain infrastructure can do to advance the markets. In terms of actual crypto assets, however, they are waiting for further regulatory certainty before moving into that space.

Technology infrastructure challenges

A broad range of critical infrastructure challenges needs to be addressed before crypto can become a fully tradeable asset class by institutional investors. The most important of which is exchange platforms that can handle trading at stock and futures exchange speeds, meaning FIX APIs will need to be implemented and standardised across crypto exchanges.

The Working Group is developing a set of best practices for crypto assets and standardised rules of engagement. Separately, a demonstration project of an exchange implemented using FIX in a high performance web based architecture was found to be relevant and suitable for crypto exchanges, as well as other venues.

Solutions for other elements of technical infrastructure that also need tackling include:

- Identification: Standardised currency and trading (ticker) symbols is an area that FIX is actively participating in, developing identification of second tier non-fiat digital currencies. Other working groups are currently addressing the creation of standard instrument identifiers for exchange listed crypto asset instruments.

- Mining power: As the crypto space evolves we are going to need to see additional investment into more energy efficient equipment to power the mining process, or variants to the blockchain that sacrifice some shared consensus for less computationally intensive approaches.

- Spot exchanges: While retail exchanges need to focus on friendly user interfaces for mostly manual trading, institutional trading needs the ability for full automation in order to increase efficiency. Many of these systems will be tied to other systems as part of an overall larger investment strategy as well as being proficient in low latency access, redundancy, use of common APIs, and overall ease of access.

- Institutional-level wallet solutions: While there are many consumer wallet solutions available in the marketplace, enterprise wallet solutions are very limited because the knowledge of capital requirements in this area is scarce. Further, any wallet solution needs to have the flexibility to adapt to the various nuances of each institution.

- Futures and Clearing: Some exchanges have launched crypto Futures and Clearing offerings, though they are very limited in scope. Volume on the US-based exchanges for Futures continues to grow, and as we experience growth we will see additional product offerings and exchanges come to the space. These products are not just important for the Spot marketplace but should also have a link to the mining community allowing them to hedge risk. To allow true hedging of risk there will need to be more contract months with liquidity offered to allow the full use of the product.

- Custody solutions: Some large custodian firms are entering the space though at a very cautious pace. Given the global nature of the crypto market, applying national custody rules will be difficult. Regarding infrastructure and ownership, especially in relation to wallets, issues around proper administration of asset custody need to be clarified, for example the difference between cloud-based hosting versus hosting via a physical cryptographic wallet hardware.

Regulatory hurdles

Regulation is perhaps the largest hurdle facing the crypto market in the eyes of institutions. Although technology moves quicker than regulation by nature, a much faster adoption of regulatory updates in this area is needed; a middle of the road mentality may be needed to allow for continued industry growth. The bottom line is regulators are seeking out experts in this space to help them better understand the marketplace. An initial Code of Conduct and taxonomy of crypto assets, as developed by the Global Digital Finance initiative, is a good example. This further understanding will allow regulators to ensure all parties can participate with a minimisation of risk as much as is possible.

Working together

The development of professional investment markets around crypto is reminiscent of the launch of the internet in the early 90’s. There was no idea then of the power it held, however in hindsight, the opportunity was like no other. A relatively simple paradigm of the world wide web unleashed an incredible global revolution and upended wealth creation and power. Crypto assets, based upon a simple model of technology-driven trust, will potentially result in an equivalent level of disruption and change in society.

It is no wonder that proponents of crypto assets believe we will eventually see a shift away from full governmental control of currencies, to currencies driven by technology algorithms similar to that of bitcoin, thus avoiding any damaging inflationary effects following times of crisis. Today, however, we are a very long way away from that scenario – crypto is not going to replace the US Dollar overnight. Simply put, we are still in the bottom of the first inning and have a long way to go on all fronts; the only way to get there is through education and working as a community to promote and grow crypto in an ethical and transparent model.

©BestExecution 2018