TURQUOISE BLOCK DISCOVERY™ FIRM UP RATES: INTEGRITY MATTERS.

Robert Barnes, CEO Turquoise

Robert Barnes, CEO Turquoise

Robert Barnes, CEO Turquoise

Robert Barnes, CEO TurquoiseAt a time of global passive indexation1 and an electronic order book environment that naturally leads to small average trade sizes2, investors that wish to outperform benchmarks are calling for innovation in electronic block trading.3

To answer this call for innovation and still trade in the presence of anticipated MiFID II double volume caps, one needs a respected and working trading mechanism that can match orders above 100% of the Large In Scale (LIS) threshold determined per stock by ESMA.

Turquoise has a working LIS innovation with demonstrable quality: Turquoise Block Discovery™ which matches undisclosed block indications that execute in Turquoise Uncross™.4,5

Turquoise facilitates electronic trading of larger orders

Turquoise midpoint dark order book is different to those of other European dark pools. Turquoise prioritises orders by size and features innovations such as Turquoise Uncross™ and Turquoise Block Discovery™ that deliver the first example of a broker neutral venue that is reversing the electronic trend of shrinking trade size. Turquoise Block Discovery™ now averages more than E200,000 per trade, and this average is more than twenty times larger than the average E10,000 for electronic trades matched by continuous dark order books.

MiFIR Article 4(1)(c) can allow dark trading for orders received by a venue that are LIS compared with normal market size and not include them in the MiFID II double volume cap calculations. This is a challenge for the current market profile where much less than 1% of trades matched on European lit order books trade in sizes greater than LIS.

Turquoise features a differentiated profile:

• 1% of Turquoise continuous matching in its midpoint dark book traded values in sizes greater than LIS; this is similar to other external dark order books.

• 2% of Turquoise overall dark book value [adding in Turquoise Uncross™ executions] trade in sizes greater than LIS.

• 20% of Turquoise Uncross™ value traded is in sizes greater than LIS.

• 50% of Turquoise Block Discovery™ value traded is in sizes greater than LIS.

The insight is that Turquoise today has a working mechanism for larger orders, including those LIS compared with normal market size.

I will now outline metrics that address the integrity of the trading mechanism.

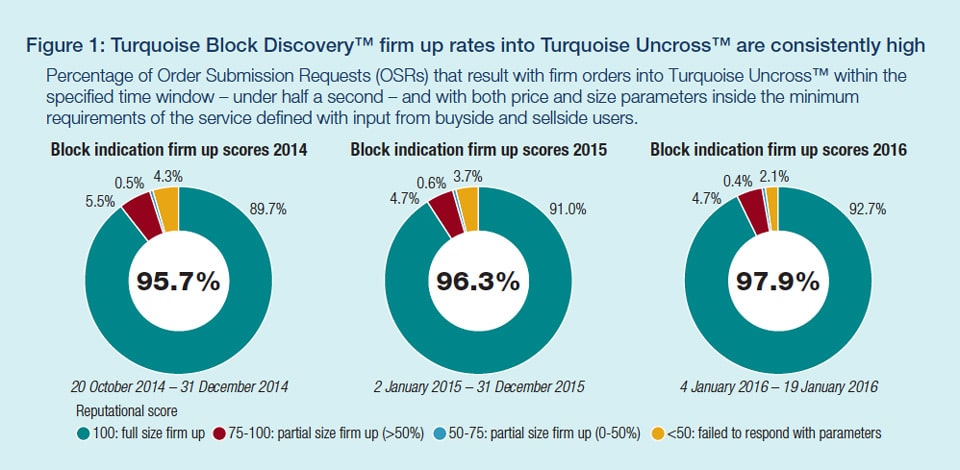

Turquoise Block Discovery™: high firm up rates and robust reputational scoring

Turquoise Block Discovery™, launched October 2014, has more than a year’s worth of empirical measurements evidencing consistently high firm up rates. These high firm up rates result from robust automated reputational scoring, which measures the difference between the original block indication and the subsequent firm order.

Since launch, more than 95% of order submission requests (OSRs) resulted with firm orders into Turquoise Uncross™ within the specified time window – under half a second – and with both price and size parameters inside the minimum requirements of the service defined with input from buyside and sellside users.

Furthermore, in more than 90% of all OSRs, the firm order met the minimum requirements and was at least the full size of the originating block indication or larger.

Figure 1 clearly shows that only in less than 5% of OSRs did the respondent fail to come back within the prerequisite core time and size parameters. The key insight from this is that the vast majority of Turquoise Block Discovery™ OSRs successfully firm up.

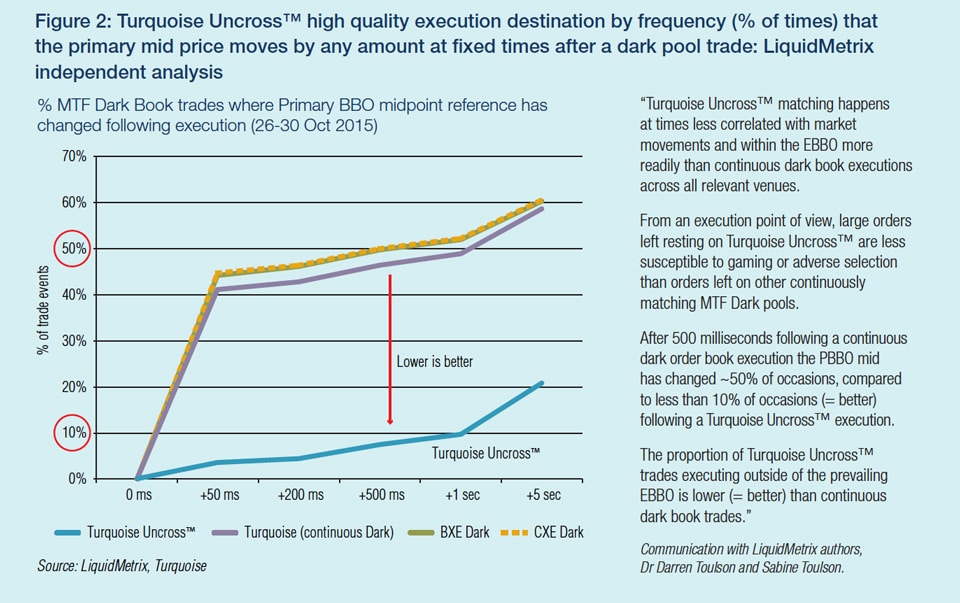

Turquoise Block Discovery™ block indications firm into Turquoise Uncross™ for execution. Turquoise Uncross™ is an innovation that provides randomised uncrossings during the trading day, ideal for larger and less time sensitive passive orders.

Turquoise Uncross™ has been the subject of multiple studies by LiquidMetrix, the independent analytics firm that specialises in venue performance metrics and execution quality analysis.

LiquidMetrix repeated its analysis in October 2015 and, for the third year in a row, spanning before and after the 2014 launch of Turquoise Block Discovery™. LiquidMetrix again concluded that trades occurring on Turquoise Uncross™ had a far lower correlation with sharp market movements on primary venues than trades occurring on other continuously matched MTF Dark Pools.6

Surveillance of Turquoise activity, including monitoring of price movements ahead of Turquoise Uncross™ is undertaken by the independent London Stock Exchange Group Surveillance team. Suspected manipulation of the reference price will be referred to the UK securities regulator, the Financial Conduct Authority (FCA).

A combination of robust automated reputational scoring, independent quantitative analysis evidencing empirical quality of the LIS trading mechanism, and an independent surveillance oversight add further to confidence in the integrity of Turquoise Bock Discovery™ for the matching of undisclosed block indications that execute in Turquoise Uncross™.

Footnotes:

1. Barnes, Robert. “European Equities: How We Got Where We Are Today”, Global Trading, Q1 Issue #53, 13 March 2015, pages 48-49. https://fixglobal.com/home/european-equities-how-we-got-where-we-are-today/

2. Barnes Robert. “Dark pools and best execution” Best Execution, Summer 2015, pages 79-81. www.bestexecution.net/analysis-dark-pools-best-execution/

3. Barnes, Robert. “Dark pools and best execution: Turquoise Block Discovery™”, Best Execution, Autumn 2015, pages 69-73. www.bestexecution.net/analysis-dark-pools-best-execution-3/

6. LiquidMetrix Turquoise Uncross™ – Execution Quality Analysis by Dr Darren Toulson & Sabine Toulson, extracts of presentation to Turquoise Block Discovery™ Buy side round table, 13 November 2015.

[divider_line]©BestExecution 2015

")