MADE IN ITALY.

Gherardo Lenti Capoduri, Head of Market HUB, Banca IMI explains why Italy is ahead of the game when it comes to best execution.

Gherardo Lenti Capoduri, Head of Market HUB, Banca IMI explains why Italy is ahead of the game when it comes to best execution.

Gherardo Lenti Capoduri, Head of Market HUB, Banca IMI explains why Italy is ahead of the game when it comes to best execution.

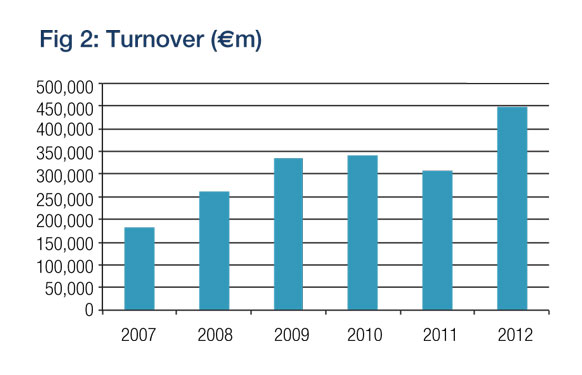

Gherardo Lenti Capoduri, Head of Market HUB, Banca IMI explains why Italy is ahead of the game when it comes to best execution.Back in 2007 in Italy, MiFID I came into effect for fixed income trading. As a result each Italian fixed income market began to compete against one another. The choice available included two regulated markets (Borsa Italiana-MOT segment and MTS BondVision), four fixed income MTFs (ExtraMOT, Hi-MTF, EuroTLX and MTS BondVision Corporate) and 17 Systematic Internalisers (SIs). It is perhaps illuminating to see how our fixed income markets have developed in the period following this regulatory change (see Fig. 1-2)

These markets target either institutional size orders or retail size orders and within their respective spaces they compete against each other by offering members:

• Different microstructures (all to all, quote driven, quote and order driven, auction, RFQ etc.)

• Different products (government bonds, corporate bonds, emerging market bonds, high yield, sovereign bonds, multi or single currency)

• Additional compliance related services (fact sheets on each instrument)

• Price

Following this change in market structure, brokers started to offer best execution in fixed income by adding smart order routing (SOR) to their execution policy, and their market-making desks started to access and capture available flow on several different markets. It is worth noting that brokers have striven to offer clients access to both market traded and OTC liquidity through creative solutions which aim at aggregating and normalizing, as much as possible, these two very different sources of liquidity. In short, the core components of this fixed income model include:

• A Systematic Internaliser

• Market memberships

• OTC – liquidity

• Sales support: Pre trade and post trade transparency – all blended and made unique with their own choice of technology.

On the market-making side, investments were made in order to compete in a more transparent environment. Both the Hi-MTF and EuroTLX successes show that there is an appetite by market-makers to provide liquidity on these markets. What is key is that in a structurally illiquid market such as fixed income, both cater to the specific needs of the market-maker by building their market microstructure around the presence of a market-maker.

Hi-MTF is only quote driven – the orders hit the market maker’s bids and offers, whereas EuroTLX is a hybrid, quote and order driven microstructure where market-makers have an obligation to be present on the book all day of a minimum size but enjoy a certain level of protection through the presence of anti-gaming rules.

Banca IMI launched Market HUB, its multi-asset electronic trading platform, in 2007. The asset classes available from the start were equities, fixed income and listed derivatives. FX was added in 2012. In fixed income, in addition to Banca IMI’s high touch service, it offers best execution and access to over 20,000 bonds by connecting to trading venues, OTC liquidity providers and offering additional liquidity on Banca IMI’s systematic internaliser Ret Lots Exchange.

European Regulation

MiFID II is expected to introduce many of the changes to the fixed income market structure already experienced in Italy. Of course, it won’t be exactly the same, and the market will not react in exactly the same way, but the main “ingredients” are there. Looking at the financial services industry in London, what we have observed in Banca IMI in the last two years is a shift from an initial resistance to the regulatory changes proposed, to, more recently, some innovative solutions being thought of and, in some cases, rolled out. What is currently being rolled out is only the beginning – solutions range from brokers setting up their own marketplaces to brokers who clearly state the need to provide clients with aggregated rather than fragmented liquidity. In our view, the second approach is more interesting for clients, especially if combined with the additional liquidity offered by the broker on its systematic internaliser.

The SI allows the broker to provide liquidity to its clients, and flow that is not captured is routed to market venues through a SOR. Dealer-to-client (D2C) venues tend to target either retail size orders or institutional size orders. In Europe the venues that Banca IMI monitors are the following:

• Retail size: BME, Stuttgart, Deutsche Börse, NYSE Euronext, NasdaqOMX/Nordics, SIX Swiss Exchange, Hi-MTF, Borsa Italiana/MOT, EuroTLX.

• Institutional size: Bloomberg, Tradeweb, MTS Bondvision, MarketAxess, Reuters TRFIT, NYSEBondMatch.

Regulatory impact

We believe that the industry, once the resistance to regulatory change has been overcome, will find innovative ways to adapt. The fact that this change takes place in a business environment in which flow is not expected to increase and margins are expected to decrease will add an edge to the creativity required in order to balance these elements.

The shift from a mainly OTC trading environment to a mainly regulated market trading environment can be compared to a “Copernican Revolution”. Overall it will introduce greater transparency and major changes such as CCPs. However, we believe that just as the planets continued to exist, so will the key components of fixed income flow within investments banks which comprise: sales/information and traders/risk. What will change is the flow generation process. Regulation will force standardization and this lends itself to industrialization and automation of processes which up until today have been labour intensive.

In this scenario, we believe Banca IMI’s Market HUB Fixed Income solution is innovative and has the opportunity to compete at the European level by offering clients a MiFID II trading environment, today.

©BestExecution | 2013